Car financing, a requisite of the auto-buying process, provides potential car owners with the financial resources necessary to acquire a vehicle. The process typically involves borrowing funds from a financial institution and agreeing to repay the loan amount, plus interest, over a specified period. This option opens up the possibility of vehicle ownership to those who might not be able to afford an outright purchase, making it an indispensable aspect of the automobile industry. Car financing is, in fact, how most Americans acquire their vehicles.

The types of car financing available are numerous and diverse, each tailored to cater to a different set of buyer needs. The purpose of this article is to demystify the often complex process of car financing, providing you with insight into the basics, the types of financing available, and what you need to know when walking into a dealership. Armed with the right knowledge, you will be able to make informed decisions that align with your financial goals and vehicle needs.

Understanding Car Financing Basics

Car financing involves borrowing a certain sum of money to purchase a vehicle. This loan is then repaid, with interest, over an agreed-upon period known as the loan term, typically ranging from three to seven years. Some key terms you’ll encounter include APR (Annual Percentage Rate), which is the annual cost of your loan including interest and fees, and down payment, the upfront amount you pay towards the purchase of the vehicle.

The loan principal refers to the original amount borrowed, while the interest is the cost you pay to the lender for the loan. Terms like loan-to-value ratio (LTV), represent the relationship between the loan amount and the value of the car. Every dealership offers different rates, so it is important to do your research. Speak with a representative from car dealerships in Orlando to find what plan works best for you.

Preparing for Car Financing

Your credit score, a numerical representation of your creditworthiness, significantly impacts the interest rate you’re offered on your loan. Lenders use this score to determine the risk associated with lending to you: the higher your score, the lower the perceived risk, and the more favorable the terms you’re likely to be offered. It’s a good practice to check your credit report for any inaccuracies and understand your score before starting the car buying process.

Next, you should determine your budget. This includes considering the total cost of owning a car, not just the sticker price. When calculating affordability, take into account insurance, maintenance, fuel, and, of course, your monthly loan payments. A rule of thumb is that your car expenses should not exceed 20% of your take-home pay. Understanding what you can afford helps ensure you don’t overextend yourself financially and can comfortably meet your loan payments.

The third part of preparing for car financing is seeking pre-approval. Pre-approval involves a lender giving you a conditional commitment to a loan amount before you start shopping. This step can be very beneficial as it gives you a clear idea of what you can afford, strengthens your negotiating position, and speeds up the car buying process. To get pre-approved, you’ll typically need to provide information about your income, employment, and some other aspects of your financial situation. A pre-approval is not a guarantee of a loan, but it’s a big step towards securing financing.

Types of Car Financing Available at Dealerships

Direct Lending vs. Dealership Financing

In direct lending, a buyer secures a loan directly from a bank, credit union, or finance company and uses that loan to pay the dealer for the vehicle. This allows the buyer to shop around for the best terms before heading to the dealership. In dealership financing, the dealer acts as a middleman, submitting the buyer’s credit application to multiple lenders to obtain financing terms.

New Car Financing vs. Used Car Financing

New car financing is for the purchase of brand new cars, while used car financing is for pre-owned vehicles. The interest rates and terms can vary between the two, with new car loans typically offering lower interest rates.

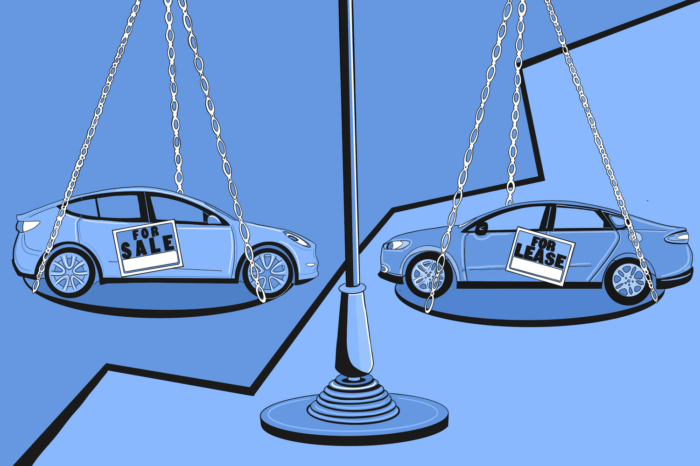

Leasing vs. Buying

When you lease a car, you’re essentially renting it for a long-term period, typically 2-3 years, after which you return the car to the dealer. Leasing usually has lower monthly payments than buying, but you don’t own the car at the end of the term. Buying a car, whether with cash or through financing, means you own the vehicle and can keep it as long as you want or sell it whenever you choose.

The car financing process can seem daunting, but with the right knowledge and preparation, it can be manageable and even empowering. Understanding the basics, preparing adequately, and actively participating in the negotiation process can help you secure favorable terms that align with your financial goals. Buying a car is a major financial commitment. Take the time to understand every aspect of your car financing options and make an informed decision that will serve your needs both now and in the future.